Need an example of a home buyer letter? Here is the one we submitted in addition to our $1.1 million offer for 614-618 Eugenia Street in San Francisco. Fingers crossed! Home Buyer Letter: July 18, 2013 Dear [Sellers], Thank you…

Money Monday: The Rigors of Getting a Mortgage in this Economy

My friend Affinity who wrote this fantastic post on retiring early, agreed to write another post on getting a mortgage in this challenging environment. She made the move from San Francisco to Oakland and had this important advice to share….

Money Monday: Missed Housing Opportunity

I have a set of housing criteria which filter out some real housing gems. One of these criteria is a parking spot which this condo in the Inner Richmond does not have. It’s already in contract and I swear if…

Money Monday: How Soon Can I Retire?

Did anyone see in the news that Bruno Mars’s Filipino mom died of a brain aneurysm…at the age of 55?! She was a dancer so I have to believe she was fit and otherwise healthy. When I hear about people…

I’m Homeless!

Well that was a downer. To watch Cal lose their lead, then ultimately lose the game was heart-breaking. Ugh. Before I get entrenched with work this week, I wanted to quickly post that we definitively sold my condo. I mentioned…

I Will Sell This House Today!

Clock is ticking, people. You don’t want to miss this opportunity to buy a walk-in closet in the heart of San Francisco for half a million dollars. I mean, seriously, who in their right mind would pass on my humble…

Money Monday: Home for Sale

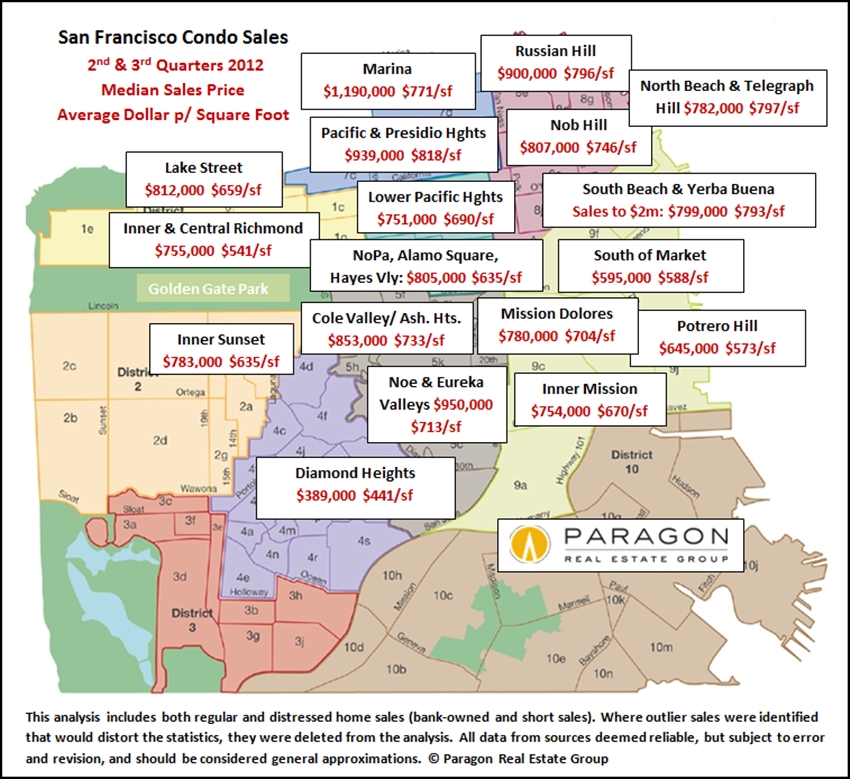

I know it’s not Monday and I’ve been delayed on my posting, but here’s why. My 1 bedroom condo in Lower Pacific Heights is now up on MLS and available for purchase! Get out your check books, people. It’s listed…

Money Monday: Landlords, Slumlords, and Me

You know how people call their landlords ‘slumlords?’ I am the opposite of that. I’ve been renting my 1-bedroom, 650 square foot condo in Lower Pac Heights since June 2009. This 3-and-a-half year time frame can be broken down into…

Chasing the Low Refi Rates

I am trying to refi my place. My last refi was unsuccessful because the appraisal was low which put me underwater, which was upsetting because I don’t believe the comps supported such a poor price. So I am at it…

Money Monday: HOAs

99% of San Franciscans can’t afford to buy a single family home unless you want to live in Bayview which may sound pretty, but most definitely is not. Instead we hoard our money to buy a little piece of the…